August 2, 2018

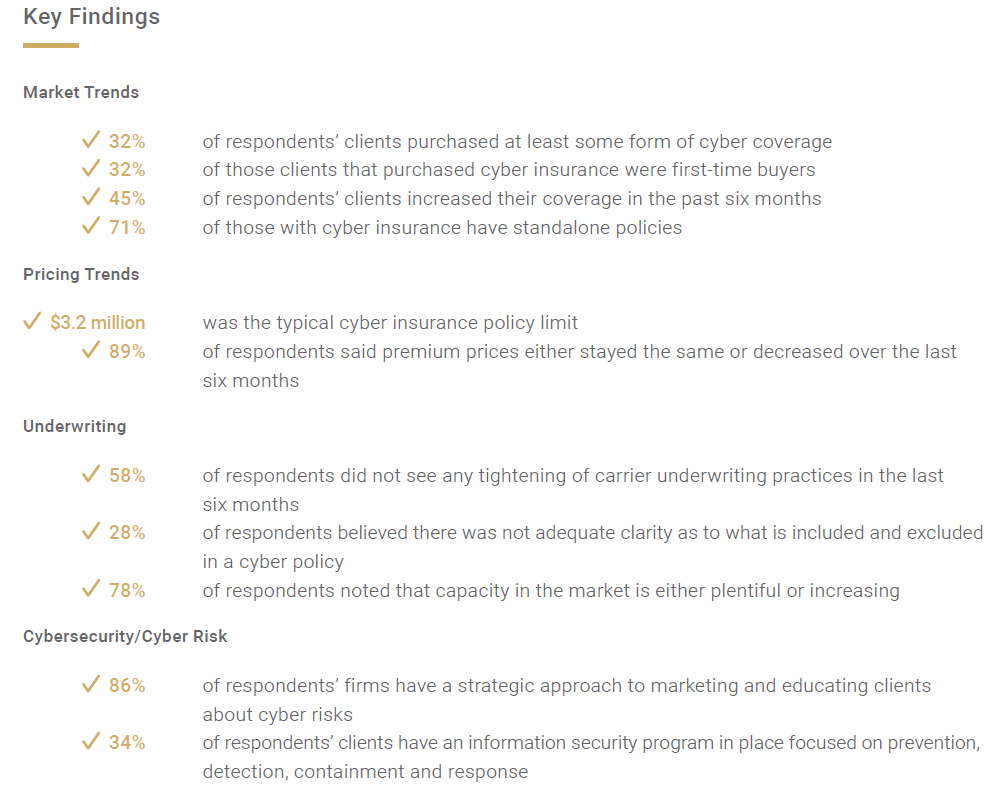

The Council of Insurance Agents & Brokers released its biannual Cyber Market Watch Survey this week. Results were consistent with responses from the first and second halves of 2017: cyber insurance take-up rate remained low at 32 percent, and 89 percent of respondents saw premium pricing stay flat or decrease over the past six months. Respondents also agreed that market capacity was plentiful, and some even noted an increase in capacity due to an influx of insurers moving into the cyber market space.

“Although brokers and their clients reported an increase in attention and awareness on cybersecurity and cyber coverage, we still have not seen that translate into an increase in take-up rate,” said Ken A. Crerar, President/CEO of The Council. “Roughly 32 percent of respondents’ clients purchased cyber coverage in the past six months marking no significant change over the past two years.”

Brokers also saw a lack of clarity in cyber policies as a persistent problem, according to results from survey. Approximately 83 percent of survey respondents said that there was either “insufficient” or only “somewhat” sufficient clarity from carriers as to what is covered or excluded in a cyber policy. As one respondent from a large national firm explained, “Terms continue to rapidly evolve on an annual basis. Carriers are using different names to describe same basic coverages which sometimes creates confusion.” “Semantics is a problem,” said another respondent, “just as everybody learned Social Engineering endorsement, we’re now seeing new wording [cyber deception, for instance], lower limits, and higher price.”

“When it comes to cyber insurance,” writes Eleanor Vaida Gerhards of Fox Rothschild LLP in an article for Property Casualty 360, “one size does not fit all.” As obvious as that may seem, a survey of C-suite executives undertaken by her firm revealed that although cyber coverage is popular, often the limitations of that coverage are poorly understood—or even not known about until a company files a claim. The overarching explanation for this, she claims, is a lack of clarity; specific examples of this lack of clarity she cites are “misunderstanding of first versus third-party limits,” incorrectly assuming a policy covers losses from “social engineering fraud,” and “unclear ‘minimum required practices’ conditions.”

The survey, which consisted of 16 questions designed to provide insights into the burgeoning cyber insurance market, creates a snapshot of the market, allowing The Council to monitor changes and trends. Drawing from a nationwide sample of brokers, it provides a unique, retroactive look at metrics relevant to members of The Council, such as premium pricing, renewal rates, and typical policy limits.

Click here for the full report.

Summer 2018 Cyber Market Watch Survey Highlights

Click here for the full report.